Information is available in 简体中文, 繁體中文, فارسی, தமிழ், Español, Português, Français, Italiano, 한국어 and over 180 languages by calling 311.

The Vacant Home Tax (VHT) program requires homeowners in Toronto to let the City know if their property is occupied or vacant by making a declaration every year. The goal of the program is to increase the supply of housing by encouraging owners of vacant residential properties to sell them or rent them out. Owners who choose to keep their properties vacant are subject to a tax, with the revenue allocated to affordable housing initiatives.

You can view the status of your Declaration, Notice of Complaint, Appeal or Audit on the Property Tax Lookup page by scrolling down to the Vacant Home Tax section.

If a declaration is not received by the April 30 deadline, the City will assume the property was vacant and send you a Notice of Assessment (Vacant Home Tax bill). Owners can dispute a bill by submitting a Notice of Complaint.

If you received a Supplementary Notice of Assessment because of an audit, you can submit a Notice of Complaint within 90 days of the date shown on your bill.

The deadline to dispute your bill for the 2022, 2023, and 2024 tax years has now passed.

The deadline to dispute your 2025 bill is December 31, 2026.

If you disagree with the decision stated in your Notice of Complaint, you may file an appeal within 90 days of the decision.

Your appeal will be heard in writing by the Appellate Authority (the City’s Deputy Treasurer). A written hearing means there will not be an in-person hearing of your appeal. It is important that you submit all required documents and evidence that support your appeal.

Once your appeal is received, the written hearing will be scheduled within 90 days of the City receiving your appeal request. A decision letter will then be issued within 30 days of the decision being made.

The decision of the Appellate Authority is final.

If your property is selected for audit, you may be required to submit further information and evidence to support your occupancy or exemption claim. If further documentation is required, you will be contacted by mail.

Once an audit is complete, you will be notified by mail of the outcome. If your property is determined vacant, a Supplementary Vacant Home Tax Notice of Assessment will be issued. You can dispute the decision of an audit by filing a Notice of Complaint within 90 days.

You may be contacted by mail and asked to provide further documentation, information or clarification about your submission. You will have 60 days from the date of the letter to submit documents to support your occupancy or exemption claim. You can submit your documents through the City’s secure online portal.

You should submit copies of only the information and documents requested. If original documents are provided, they will be retained in accordance with the Toronto Municipal Code Chapter 217. Consent should be obtained before submitting documents containing any personal information relating to any other individual. Supporting documentation must be relevant to the applicable taxation year.

Examples of supporting documentation include:

All records and documents pertaining to the occupation of the residential property or any exemption claimed must be retained for a period of no less than three years.

If you would like to report a residential property that you believe to be vacant, you can leave a voice message on the vacant property reporting hotline at 416-395-1098. Messages will not be returned. Please do not use this hotline to declare your property’s occupancy status.

The deadline to declare your property’s 2025 occupancy status has passed and the declaration portal is closed.

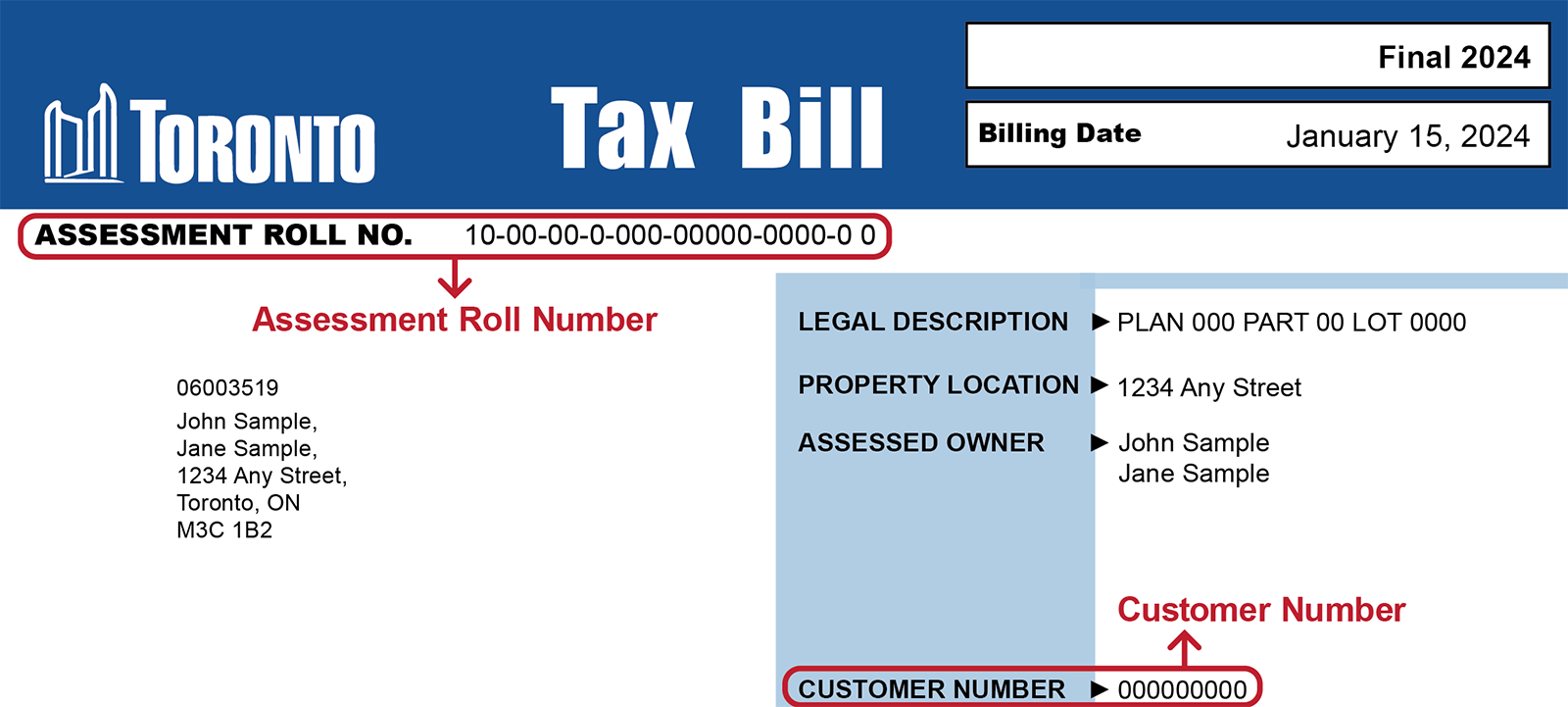

To make your annual declaration, you need your customer number plus the address or 21-digit assessment roll number from your property tax bill, property tax account statement or Vacant Home Tax notice. Declarations of occupancy status can be submitted either by the property owner or an authorized representative acting on their behalf.

You can look up the current occupancy status of your property by using the Property Tax Lookup tool and scrolling down to the Vacant Home Tax accordion

Residential property owners are required to declare the occupancy status of their property every year, even if they live there or qualify for an exemption. Most owners will not need to pay the tax as long as their declaration is received by the deadline. Owners of properties who are subject to the tax will be issued a Vacant Home Tax Notice in June 2026.

| Occupancy Status | Description | Subject to Tax? |

|---|---|---|

| Principal residence of homeowner | The property is where you live, receive mail, pay bills, etc. You can only have one principal residence. This applies even if you leave for extended periods of time due to travel or work (e.g. snow birds). To claim this occupancy status, the property must be your principal residence for at least six months of the taxation year. | No |

| Occupied by someone other than owner | This can include tenants or business tenants who must have a written agreement for a term of at least 30 days and a total of at least 6 months during the year. Other occupants such as family or friends must occupy the property as their principal residence for at least six months during the year to claim this status. | No |

| Vacant with an eligible exemption | The property is vacant due to an eligible exemption. (See eligible exemptions.) Supporting documentation is required when declaring an exemption. | No |

| Vacant | A residential property that was vacant for six months or more during the taxation year. A property will be deemed vacant if the owner fails to make a declaration of occupancy status by the deadline. | Yes |

| Situation | Description |

|---|---|

| Snowbirds and other extended-stay travellers | The Vacant Home Tax allows for owners to be away from their principal residence for extended periods of time due to travel, As long as a property remains your principal residence, you can declare the occupancy status as occupied and the tax will not apply. |

| Principal resident is away from property due to work | The Vacant Home Tax allows for owners to be away from their principal residence for extended periods of time due to employment outside the city or country. As long as a property remains your principal residence, you can declare the occupancy status as occupied and the tax will not apply. |

| Principal resident is away from property due to medical reasons | The principal resident is away from their home and receiving outpatient care at a location other than the property or the principal resident is away from their property caring for a sick family member or friend. As long as a property remains your principal residence, you can declare the occupancy status as occupied and the tax will not apply. If the principal resident is admitted into care facility or hospital for more than six months, please refer to principal resident in care exemption for eligibility criteria. |

| Residential property used for business operations | When a business is operated out of a residential unit, the property can be declared as occupied by an occupant. The definition of tenant includes business tenants. This covers situations where the owner of the property or a tenant operate their business out of the residential unit. |

| Condo units | Individual units within condominium buildings or complexes must be declared annually by their owner. Whether the tax is applicable depends on the occupancy status of the unit. |

| Owner of multiple properties | A separate declaration must be submitted for each property. |

| Newly constructed properties that are not yet assessed by MPAC | A residential property owner is required to file a Vacant Home Tax declaration only if their property is included on the annual assessment roll provided by the Municipal Property Assessment Corporation (MPAC). |

You do not have to declare if the property is:

A vacant property must be declared, but may be exempt from the tax if one of the following criteria is met:

| *Please do not provide personal medical documents or photographs as supporting documentation. | ||

| Eligible Exemption | Criteria | Supporting Documentation Required |

|---|---|---|

| Death of a registered owner | The property was vacant for six months or more in the taxation year due to the death of an owner. This exemption may be claimed for up to three consecutive taxation years if the owner of the vacant unit died in the taxation year or in the two previous taxation years. | Copy of death certificate. |

| Principal resident is in care | The principal resident of the vacant property is in a hospital, long term or supportive care facility for at least six months during the taxation year. This exemption may be claimed for up to two consecutive taxation years. | Signed letter from health care facility on letterhead; and

proof of principal residence at the subject property prior to entering care. |

| Repairs or renovations | The vacant property is undergoing major repairs or renovations, and all of the following conditions have been met:

|

Description of the project preventing occupancy, along with any supporting documents (for example, work orders, contractor receipts); and

copy of building permits issued related to the repairs and renovations (if applicable). |

| Transfer of legal ownership | The closing date of the purchased property was in the taxation year being declared. The sale involved a 100 per cent transfer of the property. This excludes name changes, adding a second owner and removing a second owner. | Copy of land transfer deed. |

| Occupancy for full-time employment | The vacant unit is required for residential purposes because the owner or their spouse is employed full-time in Toronto for at least six months during the year. The owner must have a principal residence outside of the Greater Toronto Area. | Proof of residency outside of the Greater Toronto Area; and

signed letter from employer on company letterhead, or employment contract that confirms requirement of physical presence in Toronto for the purpose of work. |

| Court order | There is a court order in force which prohibits occupancy of the vacant property for at least six months of the taxation year. | Copy of court order. |

| Vacant new inventory | New exemption beginning 2023: This exemption can be claimed by the developer of a newly constructed residential unit for up to two consecutive years if all of the following conditions have been met:

|

Sales listing from the taxation year for which the property is being declared; and

proof that the registered owner is the developer. |

| Secondary residence for medical reasons | New exemption beginning 2024: The vacant unit is required by the owner, their spouse or dependent for medical reasons, and the principal residence is outside of the Greater Toronto Area. |

Proof or residency outside the Greater Toronto Area; and

completed Vacant Home Tax Medical Treatment Certificate Form. |

Note that it’s important to provide accurate information in your declaration. False declarations of occupancy status or failure to provide information when requested may result in a fine of up to $10,000, in addition to payment of the tax.

The Vacant Home Tax has implications for property transactions, both for purchasers and vendors:

Buyers purchasing a property by way of power of sale are purchasing the property in an “as is” condition and are responsible for the associated taxes. Like property taxes, the Vacant Home Tax is attached to the property, not the individual.

Power of sale does not constitute an exemption. If the previous owner did not submit a declaration of occupancy status, the new owner is encouraged to contact their lawyer and have the vendor provide documentation to prove the occupancy or exemption status

Beginning with the 2024 taxation year, the VHT rate increased to 3% of the property’s Current Value Assessment.

Payments for the 2025 Vacant Home Tax are due in three equal instalment amounts on September 15, October 15 and November 16, 2026.

To ensure your payment reaches the City on or before the due dates, we suggest making your payment electronically through your financial institution’s online banking portal.

You can pay the Vacant Home Tax at banks or financial institutions through online banking, telephone banking, at an automated teller machine (ATM) or in-person.

To register and pay through online banking:

Payee information is subject to change without notice. For assistance, please contact your bank or financial institution.

Note that if you are enrolled in the Pre-authorized Payment Program, only property taxes will be automatically deducted from your account. Payment towards the Vacant Home Tax must be made separately.

The City accepts post-dated cheques payable to the Treasurer, City of Toronto:

Treasurer, City of Toronto

PO Box 5000, Willowdale STN A

Toronto, ON M2N 5V1

Find locations and hours of operation for the City’s Property Tax and Utilities Inquiry & Payment Counters.

You can make payment by cash, cheque, money order or debit card. If making payment via drop box, cheque or money order is accepted.

Interest charges will apply to any overdue Vacant Home Tax amount at a rate of 1.25 per cent on the first day of default and on the first day of each month thereafter, for as long as taxes or charges remain unpaid.

Upon default of payment, the unpaid amount will be added to the property tax roll for the residential property and will be collected in the same manner as property taxes.

A Dishonoured/Failed Payment or NSF fee will be applied to all payments that are not honoured by a financial institution.

False declarations of occupancy status or failure to provide information when requested may result in a fine of up to $10,000, in addition to payment of the tax.

Subscribe to receive updates about the Vacant Home Tax and reminders to submit an annual declaration of your residential property’s occupancy status and notices of important due dates.

Type (don’t copy and paste) your email into the box below and then click “Subscribe”. You will receive an email with instructions to confirm your request.

You can unsubscribe at any time.

Revenue Services collects your personal email address under the legal authority of the City of Toronto Act, 2006, Section 8 and Part XII.1, and the City of Toronto Municipal Code, Chapter 778, Taxation, Vacant Home Tax. The information will be used to inform subscribers through email about the Vacant Home Tax including reminders for important submissions dates and due dates. Questions about this collection can be directed to Manager, Customer Service, Revenue Services, 5100 Yonge Street, Toronto, Ontario, M2N 5V7 or by telephone at 416-395-1048.